Sixfold Content

Sixfold News

Meet the AI Underwriter

Sixfold is launching the AI Underwriter, an agentic colleague that does the analytical work, holds institutional memory, and tells underwriters what to do next.

.png)

Explore all Resources

Stay informed, gain insights, and elevate your understanding of AI's role in the insurance industry with our comprehensive collection of articles, guides, and more.

New Features to Revolutionize Life & Disability Underwriting

Our latest Life and Disability AI-powered features focus on overcoming longstanding underwriting challenges and gives a fresh perspective to underwriters.

With our latest product update, we’ve sharpened our focus on Life & Disability via a suite of AI-powered features that overcome common underwriting challenges.

Sixfold’s number one superpower is to easily–and quickly–ingest carriers’ unique underwriting guidelines and automatically surface the submissions that match the carrier’s unique risk appetite. Moreover, the platform empowers Life & Disability carriers to streamline the underwriting process by:

🔘 Ingesting data from multiple disparate sources in an instant

🔘 Generating a comprehensive summarization of the applicant's health history and lifestyle within minutes

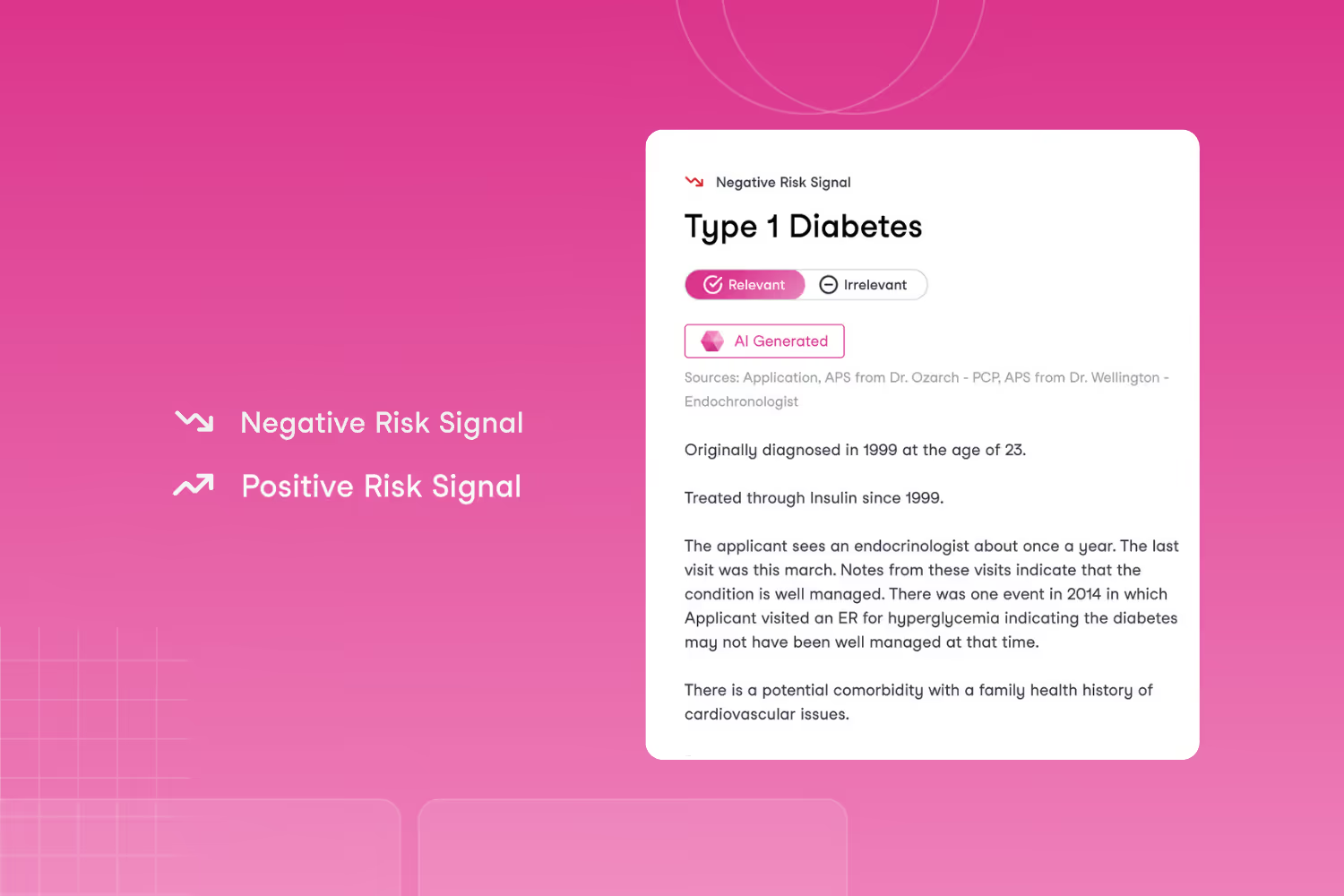

🔘 Surfacing positive & negative risk signals aligning with the unique risk appetite of each carrier

🔘 Triaging submissions with an underwriter-facing dashboard for improved resource allocation

We've significantly broadened our Life & Disability offerings by expanding into six key areas, facilitating us to quickly create a comprehensive 360-degree applicant profile in just minutes by:

✔️ Reducing manual workload through improved document ingestion

Our technology has been significantly enhanced to process and analyze an extensive history of lab results, diagnoses, and medication records, covering years or even decades.

The platform is proficient in ingesting data from various sources including APS files, MIB reports, labs, applications, supplementals, Electronic Health Records (EHR), and Fast Healthcare Interoperability Resources (FHIR) files. By automating the ingestion of these diverse data types, Sixfold eliminates the need for manual document handling by underwriters.

✔️ Refining risk evaluation with a holistic view of medications, treatments, lifestyle choices, and family history

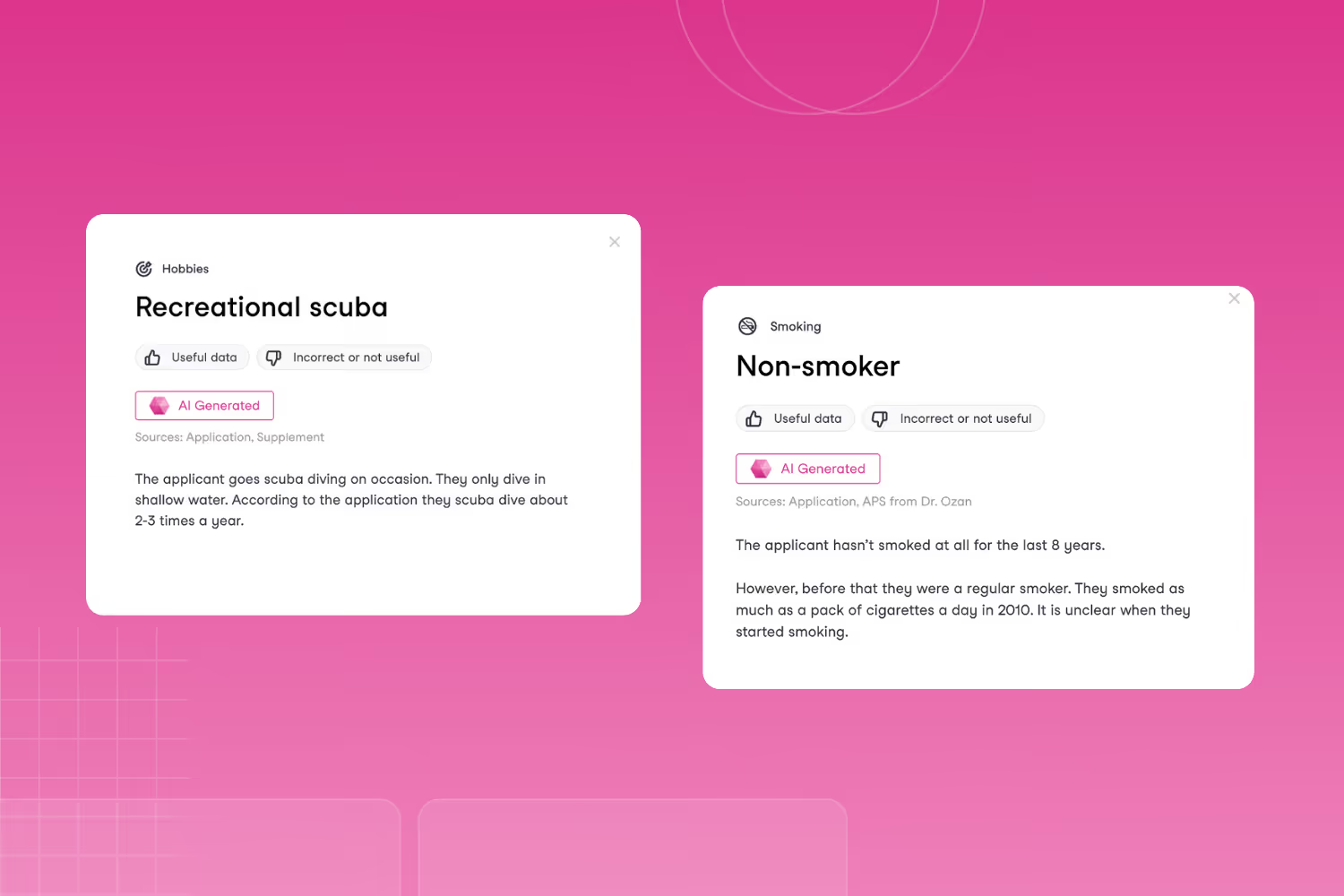

The platform leverages advanced synthesis of adjacent applicant history information, including pertinent family medical histories and lifestyle attributes, to offer a comprehensive understanding of their broader health habits and disease predispositions.

By integrating details from submitted records—such as family diagnoses ("father was diagnosed with melanoma at 63, but was successfully treated")—with insights into exercise routines ("engages in moderate-intensity aerobic exercise and weight lifting"), hobbies ("applicant scuba dives several times per year"), and substance use ("consumes a few beers every few days"), Sixfold provides a holistic view of an applicant's health.

This comprehensive approach enhances the precision of assessments, enabling more informed decisions regarding risk.

✔️ Improving risk decision precision with in-depth analysis of health condition progression

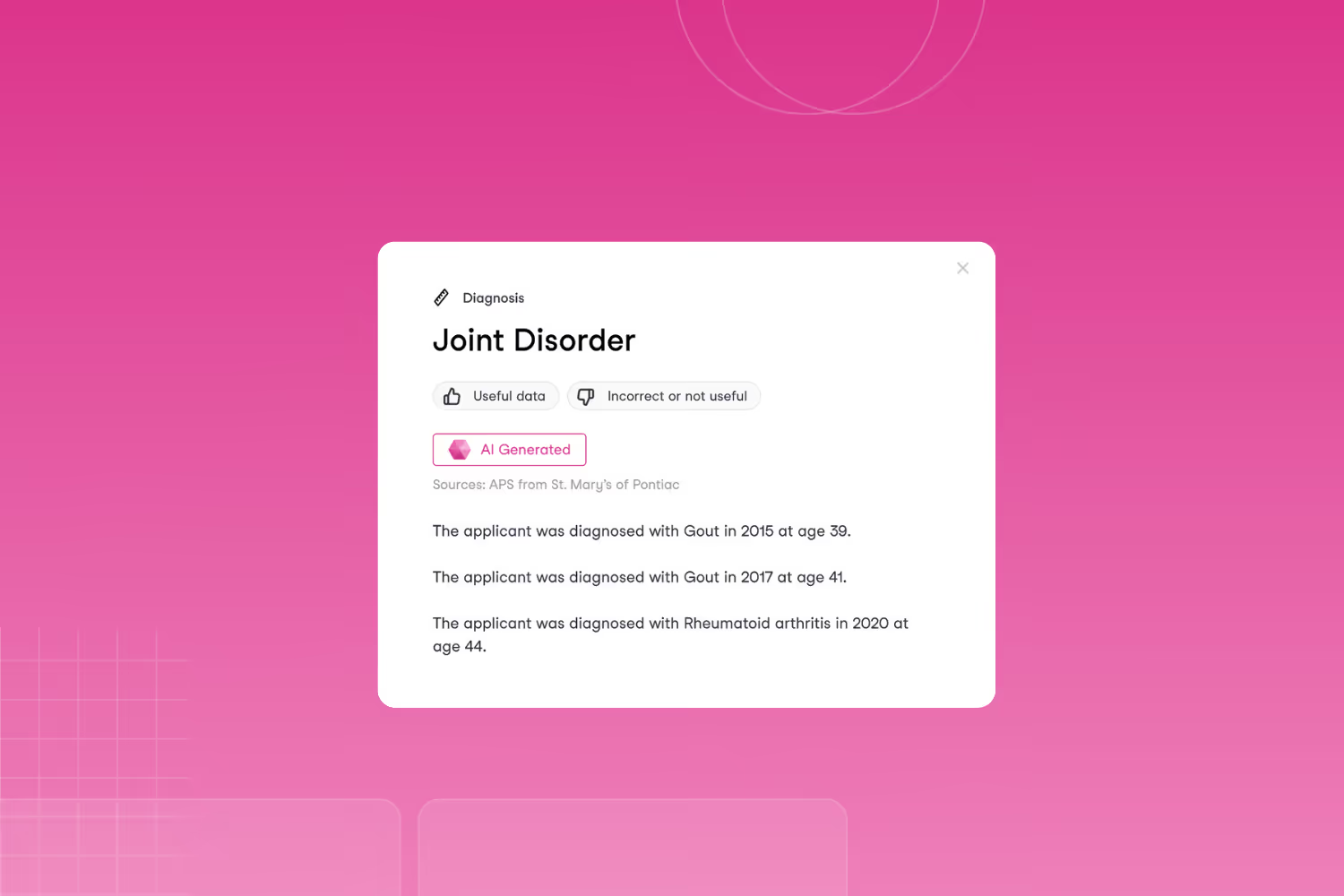

We are now able to aggregate data related to a condition, including adjacent factors like medication, to chronologically track the comprehensive progression of the condition across multiple data sources. By utilizing detailed health data and its evolution over time, we enable more informed and accurate underwriting decisions.

This approach provides a unique layer of detail, incorporating crucial health information over time, allowing underwriters to quickly grasp risk with relevant context, thereby informing more precise rating and pricing.

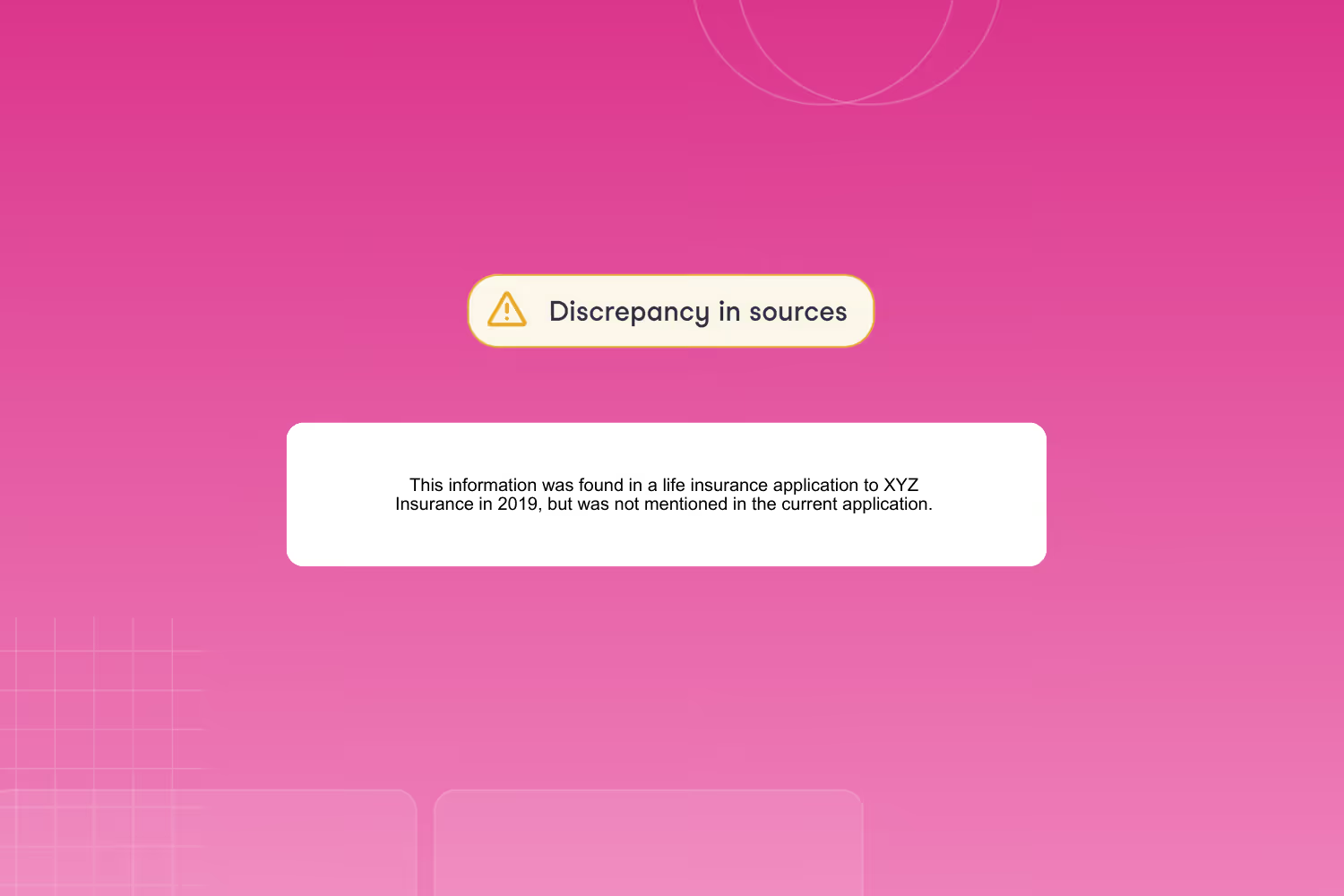

✔️ Enhancing fraud detection by identifying inconsistencies across sources

Underwriters are tasked with synthesizing and managing a vast amount of information from lengthy documents, including Attending Physician Statements (APS), self-reported data, laboratory results, and more. An important aspect of analyzing these documents is to identify inconsistencies or discrepancies that could arise from oversight or fraud. Instead of solely relying on underwriters to detect irregularities across diverse documents, Sixfold proactively identifies and flags these discrepancies to the underwriter.

The platform's automated capability to identify problematic areas empowers underwriters to make informed decisions, leading to more accurate pricing of premiums and greater reliability of applicant information, safeguarding both insurers and applicants.

✔️ Expanding traceability with full document and page number sourcing

Our recent achievement of SOC 2 Type 2 certification underscores our commitment to being a responsible AI solution.

In this release, we've taken traceability to the next level by ensuring underwriters have access to complete information sourcing, pinpointing the exact document and page for increased transparency and accuracy.

✔️ Boosting underwriting capacity with upgraded triaging functionality

Sixfold's latest update introduces a streamlined dashboard experience, designed specifically to empower underwriters to efficiently prioritize applicants who meet their risk tolerance and gracefully set aside those who do not. This effectively addresses the common 'front door issue' in Life & Disability underwriting, which involves managing an overwhelming influx of submissions by automating the pre-processing of applications. Within minutes, Sixfold accurately identifies and aligns applicants with the carrier’s risk criteria, significantly easing the burden of manual sorting and enabling underwriters to focus on the most suitable cases.

Our newest updates equip life & disability underwriters with a complete, clear and accurate health snapshot for every applicant, pinpointing key data points without sacrificing our commitment to compliance and data privacy.

Curious to see it all live? 👉 Watch our 20-minute product demo.

Exploring Tech Tools, Culture, and AI with the CTO

Discover the tech journey of Brian Moseley, Co-Founder and CTO at Sixfold, as he shares his experiences and passion for the Sixfold AI underwriting platform.

Dive into our Q&A with Brian Moseley, Co-Founder and CTO at Sixfold. We're chatting about his tech journey, from the early days at Sega to his recent tenure at American Express, and what led him to Sixfold. Brian also shares insights into the team's 'chill, pragmatic, and adaptable' culture and talks about his passion for Warhorn, his own gaming community project.

What’s your career path and how did it lead you to becoming Sixfold's CTO?

My software career began in college when I joined my friend’s community and media startup; we were among the first to experiment with web-based advertising. Through this venture, I met many tech professionals in San Francisco, who got me excited about the emerging web scene there. Ultimately, I decided to leave school and move across the country to work at Sega of America, focusing on database administration for their website.

From there, I joined several early-stage startups, including Critical Path, where I was the 17th employee. I experienced growth through its IPO, becoming an engineering manager and software architect. Later, I worked at the Open Source Applications Foundation, implementing a number of obscure internet protocols as the lead of an open source calendaring server.

As my career progressed, I found myself being the first engineering hire at a startup and then the first employee of another, so the logical next step was to become a cofounder and the CTO of Hoodline, a hyperlocal journalism company. Unfortunately, we did not succeed in reinventing local news, so I decided to try my hand at a big company and started working for American Express.

I made the leap to full-time engineering management at Amex and eventually spent five years as the firm’s Head of Developer Experience, serving a global crew of 10,000 software engineers. Working in a big company was an incredibly educational part of my career, but I increasingly had the itch to build something from scratch again. So, Alex’s pitch got my attention and ultimately led to me cofounding Sixfold AI.

What originally attracted you to Sixfold?

It was a combination of three things:

1️⃣ I’d been looking for some time for an opportunity to build a company, team, and product from scratch.

2️⃣ I had a great time working with Alex briefly back in the early 2000s, so the prospect of cofounding with him was super appealing.

3️⃣ It seemed like exactly the right moment to go after the opportunities unlocked by generative AI in vertical business domains. Everything I saw was focused on LLM infrastructure and tooling, but nobody was talking in public about using generative AI to solve problems for business users like insurance underwriters.

How is Sixfold different from other players in the field?

We aren’t encumbered with legacy technology, organizations, or ways of working. We’re building our team and product from the ground up, which means we get to experiment freely and iterate quickly.

Another aspect that sets us apart is our commitment to ensuring our product is something users look forward to, not something they complain about with each use. The complexity and challenging nature of many enterprise software interfaces can be daunting. That's why we focus on user-friendliness and intuitive design.

We value user delight! Sixfold is not only effective; it's also fun to use.

What aspects of Sixfold and its technology are you most passionate about and find particularly exciting?

I love all of my children equally 🙃

That said, as you might expect, I’m engrossed in the rapidly developing craft of generative AI engineering. What we’re doing goes way beyond basic “chat with your document” scenarios. We have a whole new set of primitives to assemble into complex systems - and they are evolving so fast it’s hard to keep up! It’s particularly interesting to apply these techniques in near real time as part of the live user experience.

Our AI pipelines are hybrids of batch and streaming, with the work distribution and scheduling needs of batch processing and the resiliency and throughput of a real-time system. “Notebook AI” solutions don’t scale or meet our availability and performance requirements without a lot of additional engineering.

How would you characterize the dynamic and strengths of the team?

Our founding team has so much experience starting and scaling companies, we’ve all done zero to one many times. That doesn’t mean we don’t make mistakes, but they tend to be new mistakes, not many of the ones we’ve seen before. And my co-founders are teaching me everything there is to know about insurance.

The core of our tech team is a group of veteran startup hands with deep experience in their functional areas who can all flex into team building and leadership as we grow. We built on this core with a group of 'smart and gets things done' engineers who can build fast and iterate quickly, especially the closer they get to the AI layer of our stack.

Ultimately, our tech team is able to build, test, and learn quickly while keeping the quality bar high. And our go-to-market team keeps us oriented, fusing an understanding of what our customers need with a compelling vision for the future of underwriting.

How do you contribute to the team's growth and development?

As a hands-on-keyboard software engineer for nearly 30 years, I lead our product and platform development from the front. I pair with our engineers to help them develop their core software skills, which include architecture, design, coding, troubleshooting, and operating in production. This also provides an opportunity for them to build mentorship skills, as there is much I can learn from them as well.

I strive to create opportunities for our team members to step outside their comfort zones. Most of our engineers arrived with a specialization in some technical area, whether it be front-end development, infrastructure, or AI. However, our team is most effective when any member can work on any feature, regardless of where it falls in our stack. Therefore, I encourage each engineer to become proficient in all our languages and frameworks. For example, an AI engineer might make changes to our core domain model in Ruby, or a front-end engineer could add a new step to our AI pipeline using Python.

What is an achievement you are particularly proud of that the team has accomplished since the launch?

I’m most proud that we’ve been able to make the product work the way we envisioned it. It’s not just about our accuracy, which is great and getting even better. Remember the first time you experienced the magic of ChatGPT? Underwriters have that same feeling when they use Sixfold AI. They don’t have to read a hundred pages of tedious documents anymore just to find the three hidden nuggets that show the risk in an insurance case. They can sit back and let Sixfold find the nuggets for them in a matter of minutes. Magic!

In three words, how would you describe the team's culture?

Chill. I don’t mean we’re not working hard or that we don’t have high intensity about our venture. But you can tell that most of us have been in startups before because people handle the pressure really well. Nobody’s freaking out or creating negative vibes. We all have each others’ backs.

Pragmatic. We aren’t striving for the perfect user experience or the most scalable systems right out of the gate. We’ll get there over time as we prove our right to be in business by delivering things customers want to pay for. We push ourselves to make “two-way door” decisions a little bit faster knowing that we can always iterate or reverse course later.

Adaptable. We develop in quick sprints and frequently stop to check in on what’s most important right now. Some weeks, that’s building features. Others, it’s improving resilience or shoring up security. At this stage of the company, every next customer engagement brings new problem statements and requirements. While we’ve introduced a measure of longer-term planning, we’re still keeping our heads on a swivel (as my high school football coach would say) to make sure our vision, roadmap, and near-term development plans evolve in the face of constant market discoveries.

How do you stay updated with the advancement in AI and LLMs, any particular newsletters or blogs that you like to follow?

I read 'Ben's Bites' daily, a resource recommended by Alex (our CEO) when I first joined. It's even included in our welcome email to all new team members. In addition, I follow 'The Information', particularly their newsletter 'AI Agenda', which I find very insightful and full of links to deeper reading.

Our team is also a significant source of discovery. Team members are constantly tuned into various niches and aspects of our industry, sharing relevant links and resources in Slack. We’re reading each other's stuff all the time.

Could you share some of your favorite tech tools or frameworks that you rely on heavily?

iTerm and Visual StudioCode - This is where I write and run my code. Others love their all-in-one commercial IDEs, but I do just fine with these tools.

Ruby and Rails - I’ve been building Rails apps and writing scripts and command line tools in Ruby since 2007. It just keeps getting better! I spend a lot of time with JavaScript as well, and it’s fine, you can’t really get away from it in the modern world, but I’ll always reach for Ruby when I can.

React - Again, I have been doing it since near the beginning, and it still scratches the itch. Haven’t had any reason to embrace the Hotwire part of the Rails omakase experience or to dabble in any of the post-React web frameworks. Maybe somebody out there will finally make me see the light?

Linear - Modern project management for product development that strikes an almost-perfect balance between the “all batteries in the universe included” and “bring your own batteries” approaches of pretty much everything else out there.

Mermaid - Being able to create a diagram by writing code has 10 x'ed my output of diagrams, which improves the clarity of my engineering dialogues.

Do you have a favorite AI solution that you would like to highlight?

Not yet! The gen AI ecosystem is still immature and changing rapidly. The popular tools and frameworks don’t always prioritize qualities we require for production usage - stable APIs, for example, or the ability to bring your own observability tools or work distribution systems. We’re having a better experience stripping down to the basics and devising our own abstractions over AI primitives (model and vector store APIs, for example) and in-house utilities.

Ask me again in 12 months - I may well have a different answer!

Any fun tech projects that you're working on at the moment (non-Sixfold-related)?

Yeah, there are two main things I'm focusing on outside of work. Firstly, I've recently picked up World of Warcraft again after about a year's break. It's been a fun way to spend time outside of building our company.

More to the point, I started a website back in 2001 called Warhorn, which I'm still running today, more than 20 years later. It's essentially a marketplace for tabletop role-playing games, board games, collectible card games, miniatures, word games, and more. I originally created it out of my love for tabletop role-playing, particularly tournament-style games like Dungeons and Dragons. It was born from the need to streamline the logistics, scheduling, and signups for large gaming events.

The site was initially written in PHP in 2001, then I rewrote it in Ruby on Rails in 2011 and added a React front end around 2016 or 2017. Warhorn has been my laboratory for learning new technologies, such as GraphQL. It's a SaaS offering, which has helped me familiarize myself with various cloud providers and vendor systems. This experience has directly influenced my decisions at Sixfold and at previous jobs.

Warhorn is not just my tech lab but also my way of contributing to the gaming community. It's a long-standing project with over 25,000 monthly active users. I've kept it running as a passion project, not for commercial purposes. It's a creative outlet for me, similar to painting on canvas. It's an enjoyable aspect of my life where my profession and hobby intersect, providing a way to relax and be creative.

Are you excited about the opportunity to work at Sixfold?

It Takes You Months to Train AIs? You're Doing It Wrong

Discover the power of AI underwriting with Sixfold - the ultimate solution to overcome traditional limits and stay ahead in the insurance industry.

It’s impossible in 2024 to be an insurance carrier and not also be an AI company. In this most data-focused of sectors, the winners will be the organizations making the best use of emerging AI tech to amplify capacity and improve accuracy.

This is a challenge and opportunity that Sixfold is uniquely suited to address thanks to our decades of collective industry and technological experience. We know insurers’ needs—intimately—and understand precisely how AI can overcome them.

In previous posts, I’ve described how Sixfold uses state-of-the-art AI to ingest data from disparate sources, surface relevant information, and generate plain-language summarizations. Our platform, in effect, provides every underwriter with a virtual team of researchers and analysts who know exactly what’s needed to render a decision. But getting there is the rub. Training AI models (these “virtual teams”) to understand what information is relevant for specific product lines is no small task, but it’s where Sixfold excels.

To use AI is human, to create your own unique AI model is divine

Underwriting guidelines aren’t typically encapsulated in a single machine-readable document. They’re more likely to exist in an unordered web of internal documents and reflected in historic underwriting decisions. Distilling a diffuse cultural understanding into an AI model can take months using a traditional approach, but with Sixfold, it can be accomplished—and accomplished well—in as little as a few days.

Sixfold’s proprietary AI captures carriers’ unique risk appetite by ingesting a wide variety of inputs (be it a multi-hundred-page PDF of guidelines, a loose assortment of spreadsheets, or even past underwriting decisions) and translating it into an AI model that knows what information aligns with a positive risk signal, a negative one, or a disqualifying factor.

With this virtual wisdom model in place, the platform can identify and ingest relevant data from submitted documents, supplement with information from public and third-party data sources, and generate semantic summaries of factors supporting its conclusions—all adhering to the carriers’ unique underwriting approach.

Frees human underwriters to do uniquely human tasks

It can take years for a human underwriter to master underwriting guidelines and rules, but that doesn’t mean human underwriters are no longer needed–quite the opposite. By offloading the administrative bulk to AI, underwriters can use their increased capacity to prioritize cases that align with their unique risk appetite.

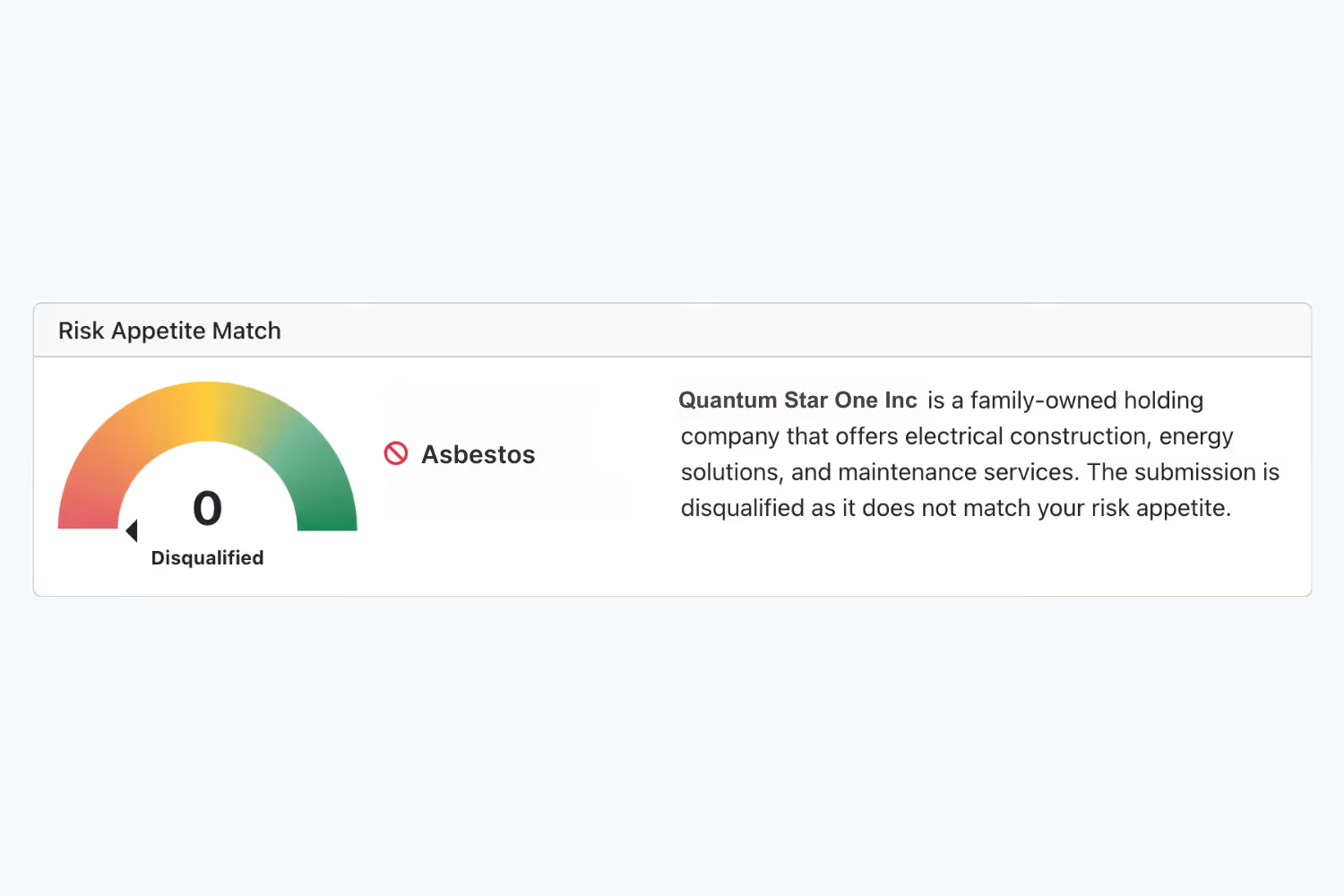

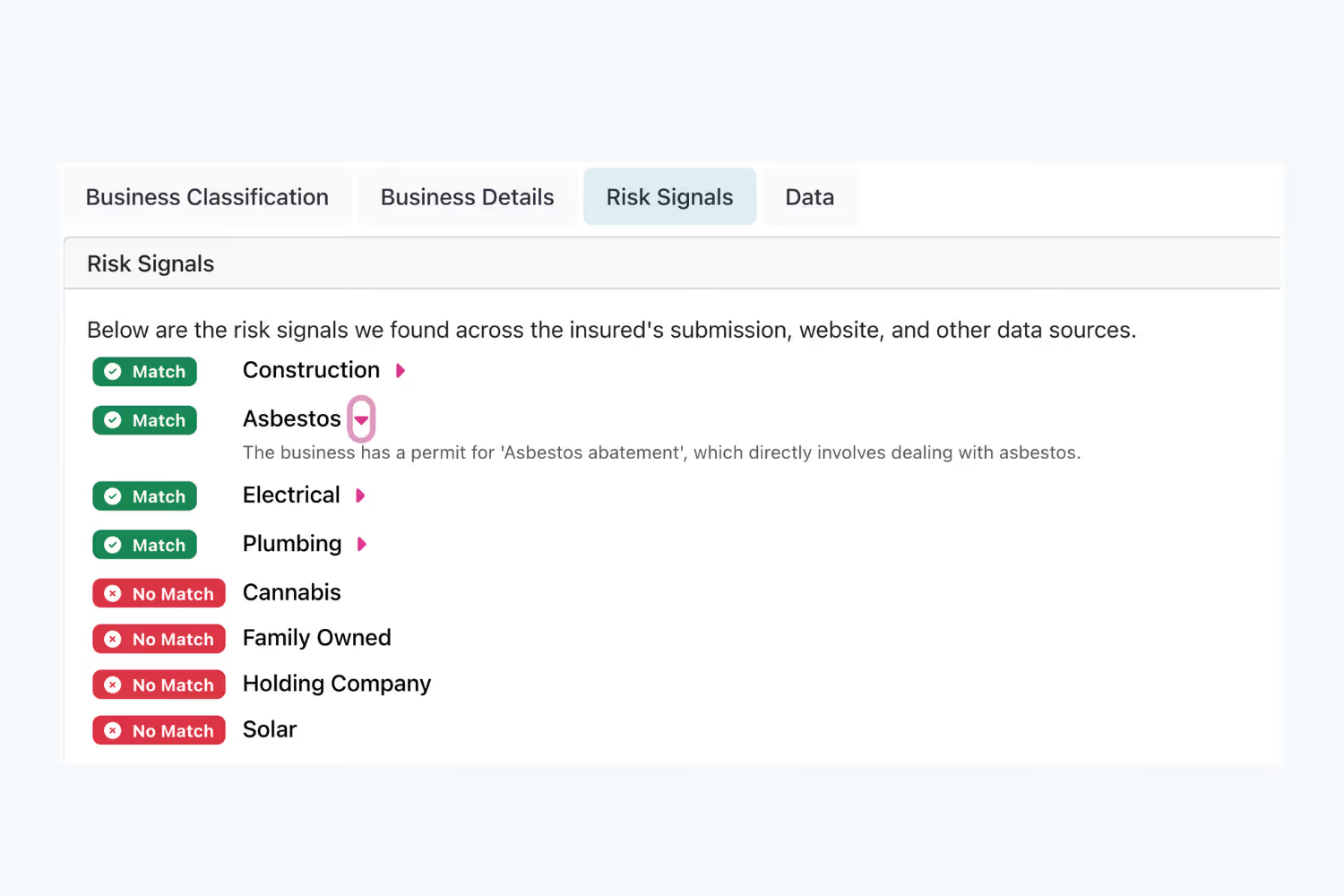

Consider a P&C carrier that prefers not to underwrite businesses that work with asbestos. When an application comes in, Sixfold’s platform processes all broker-submitted documents and supplements it with relevant data ingested from public and third-party data sources. If Sixfold were to then surface information about “assistance with obtaining asbestos abatement permits” from the applicant’s company website, it would automatically mark the finding as a negative risk signal (with clear sourcing and semantic explanation) in the underwriter-facing case dashboard. With Sixfold, underwriters can rapidly discern the applications that are incompatible with their underwriting criteria and quickly focus on cases aligned with their risk appetite.

Automating these previously resource-intensive data processing workflows allows carriers to obliterate traditional limits on underwriting capacity. The question for the industry has rapidly moved from “is automation possible?” to “how quickly can we get it implemented?” Sixfold’s purpose-built platform empowers customers to leapfrog competitors relying on traditional approaches to training AI underwriting models. We get you there faster–this is our superpower.

Sixfold Joins Guidewire Insurtech Vanguards Program

Explore the partnership between Sixfold and Guidewire's Insurtech Vanguards program, revolutionizing the industry with an AI-powered platform for underwriters.

New York City, January 9, 2024

Sixfold, the Generative AI exclusively built for insurance underwriters, today announced that the company has joined Guidewire’s Insurtech Vanguards program, an initiative led by property and casualty (P&C) cloud platform provider, Guidewire (NYSE: GWRE), to help insurers learn about the newest insurtechs and how to best leverage them.

Jane Tran, Co-founder & COO at Sixfold, expressed, “Guidewire stands as the industry's foremost policy vault, embodying the definitive source of truth. Collaborating with Guidewire empowers us to advance our enterprise-grade generative AI solutions tailored specifically for underwriters.”

Insurtech Vanguards is a community of select startups and technology providers that are bringing novel solutions to the P&C industry. As part of the program, Guidewire provides strategic guidance to and advocates for the participating insurtechs, while connecting them with Guidewire’s P&C customers.

Sixfold seamlessly handles the ingestion, routing, classification, and summarization of submissions, and provides trustworthy, data-driven policy recommendations to underwriters in a user-friendly format.

About Sixfold

Sixfold brings the power of generative AI to the underwriting process. The platform significantly reduces manual workload for underwriters and amplifies confidence in every underwriting decision with improved accuracy, transparency, and capacity.

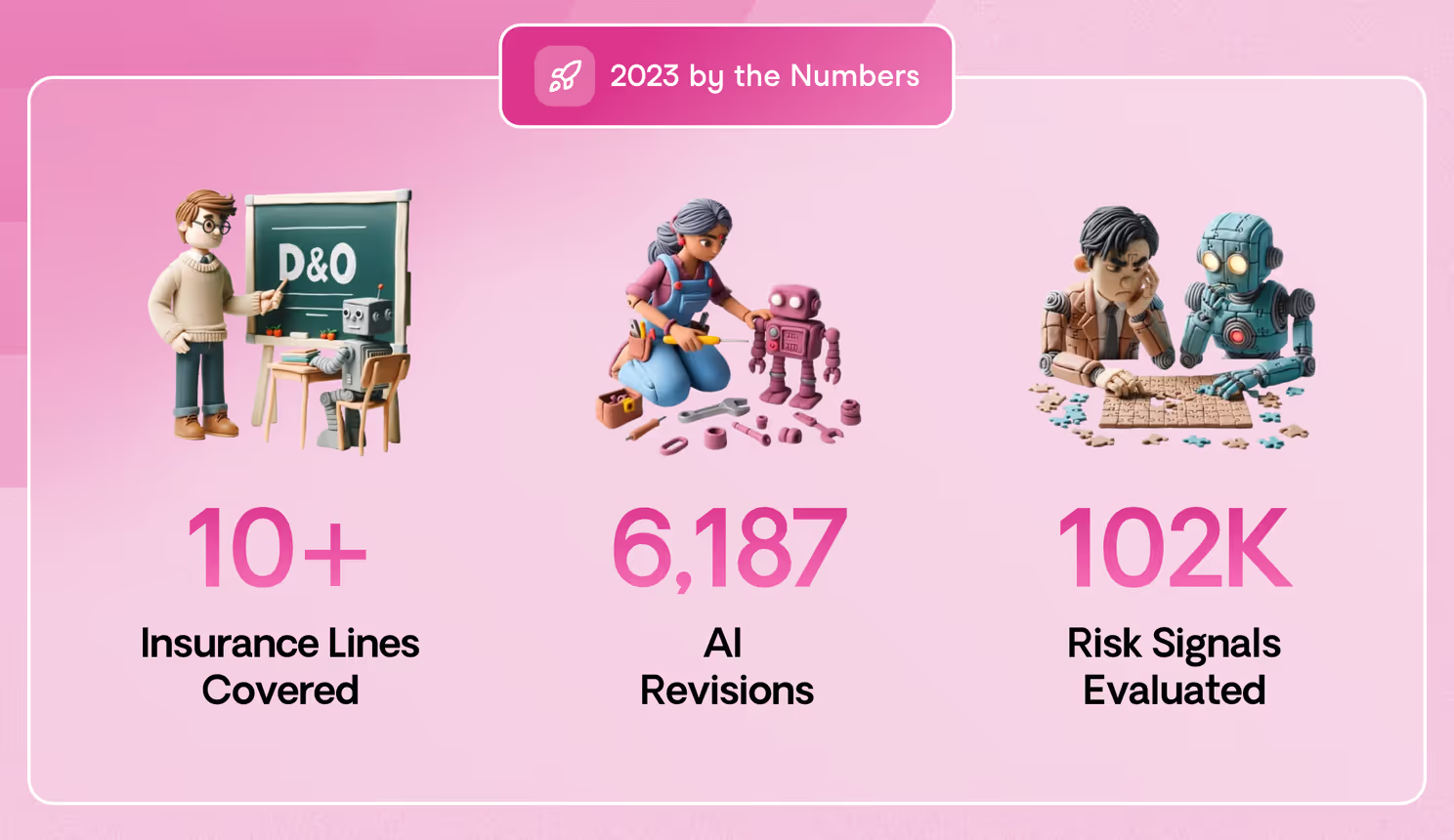

Sixfold’s Remarkable First Seven Months

In less than a year, Sixfold has transformed insurance underwriting using emerging AI technologies. Here’s how we did it.

This time last year, Sixfold was little more than a name and a vague concept. But since officially launching in May, this remarkable team (now 17-strong and growing!) has revolutionized insurance underwriting. That’s a bold statement from a biased observer, but I think I can back it up.

First, let’s briefly explore the state of affairs coming into 2023.

Modern carriers process vast amounts of data from a wide array of sources to inform underwriting decisions. Today’s competitive advantages are secured—or lost—based on the efficiency and accuracy with which one handles this data.

Over the years, multiple data-tech vendors have promised to help carriers keep pace, but they haven’t been even close to sufficient. Meanwhile, data ecosystems have grown more expansive and the tools gap, more glaring.

At Sixfold, we saw this challenge compounding by the day—not for lack of trying, but for lack of imagination. It’s what inspired us to develop a new approach that prioritizes transformation over iteration.

Our platform was uniquely built to accelerate the bewilderingly complex process of modeling risk appetite, no matter the starting point. Is your risk tolerance detailed in a loose assortment of PDFs? An Excel document? Or just a bundle of past submissions? We can make sense of it all. And that’s just the start. Our proprietary generative AI engine ingests applicant data from disparate sources at scale and—unlike traditional “intelligent” data processing tools, which merely extract data—generates clear summaries, fully aligned with carriers’ appetites, empowering underwriters to move with unprecedented accuracy and speed.

And it’s been effective. Ridiculously effective. Let’s run through a few quick examples:

✅ A leading general liability carrier was averaging 4 hours for its submission-to-quote cycles, but once they implemented Sixfold, that time was slashed to just 4 minutes.

✅ Last year, a large global cyber carrier measured its submission-to-quote cycles in weeks; now they do it in 3 minutes and 24 seconds.

✅ Before adding Sixfold to its tech stack, a major life & health carrier needed days to extract, surface, and package relevant data from multiple sources for a single life insurance application. Now the entire process is handled automatically in a fraction of the time.

Perhaps you can see where the industry is headed and why this is the area where Sixfold is focusing.

The journey from there to here

The progress our engineering team has made over this not-even-a-full year has been nothing short of astonishing. Gen AI is moving forward at warp speed–and Sixfold is moving even faster.

In just the past few months we’ve transitioned from relying on a single LLM vendor to tapping and training a plethora of platforms based on their unique abilities. Additionally, we’ve tailor-built our own proprietary AI models to increase speed, accuracy, and privacy—we’ll be tripling down on our internal R&D efforts in the years ahead. (As a side note: I can’t wait to show you what our engineers have been working on…more on that during our January webinar.)

The only thing evolving faster than AI technology is society’s views of it. More people are voicing concerns about the potential negative impact of AI, particularly around issues of scaled bias. We get it. We have a shared interest in ensuring that AI is deployed with a human-first approach.

Sixfold has been proactively and uniquely engaged in the conversation. I, and other Sixfold leaders, have repeatedly met with the state regulators and commissioners throughout the year to better understand their concerns and thinking. These meetings have helped us design our platform in anticipation of new regulations and, conversely, offer our unique insights to influence the formation of emerging rules that will allow AI to work better for everyone.

Hello, 2024

We’re exclusively obsessed with insurance underwriting. We have been from the beginning and we will continue to be in the future.

I’m beyond proud of what this team has accomplished over the past 7 months, and I can’t wait to share with you what’s in store in 2024. Join us this coming January for our first-ever virtual session, Boost Underwriting Capacity in 2024: Discover the Sixfold Impact, for a demo of how our platform enhances underwriting capacity in P&C, Life, and Specialty insurance sectors.

None of this would have been possible without the support and backing of Charles Birnbaum and Jeremy Levine at Bessemer Venture Partners, and Jonathan Crystal and Stephen McGovern at Crystal Venture Partners. We’re grateful for our bold customers and partners who understood our vision and joined us on the first leg of our journey. And of course, I can’t say enough about the Sixfold team including my co-founders Jane and Brian as well as our growing lineup of researchers, innovators, and visionaries: Brooke, Drew, Emil, Gregg, Ian, Lana, Laurence, Leonardo, Lucas, Maja, Marie, Omeed, Stewart, and Ryan.

Don’t miss our 2023 recap. See you all next year!

This post was originally published on LinkedIn.

Q&A on Generative AI in Insurance With Our AI Engineer

Explore the world of generative AI in insurance and marketing with Drew Das, AI Engineer at Sixfold, who offers advice for aspiring professionals.

We recently conducted a Q&A with Drew Das, AI Engineer at Sixfold. Our discussion covered various topics, including the nuances of developing generative AI tools for marketing versus the insurance sector, advice for those aspiring to enter the field, and tools he enjoys using.

Let's start with your background and how you got into the world of AI?

I've always been in tech. I started in web development during high school, launching a business creating WordPress sites. I studied at UC Davis, where I also worked in the college IT department. I've spent nearly 10 years working in Silicon Valley, primarily in web development.

My first introduction to conversational interfaces was in 2017 with a company focused on chatbots. This early experience involved developing chatbots for job applications, targeting sectors like truck driving and foreign workers. We aimed to simplify the application process for those uncomfortable with traditional job sites.

I've also worked in cybersecurity, food delivery, and at Jasper, a startup in generative AI. At Jasper, I was the lead of content and involved in launching Jasper Chat, a chatbot product developed in under four days. This product became a primary feature for users. I also worked on an AI-based text editor, a first-of-its-kind product that helped introduce many to generative AI.

Could you describe in your own words what an AI engineer does? Specifically, what are your daily tasks and responsibilities?

The role of an AI engineer is still evolving, as AI is a relatively new field. Previously, we had machine learning engineers and software engineers with distinct functions. Machine learning engineers focused on training computer systems for making predictions using statistical methods. Software engineers, on the other hand, worked on translating business logic into application code, often using APIs provided by the machine learning team.

An AI engineer's role is broader than that of a machine learning engineer. It involves working with various AI tools, like ML models, vector databases, and advanced techniques. An essential skill for AI engineers is prompt engineering and understanding how these systems integrate. The primary objective is to combine these systems to create software that operates on top of data, rather than just converting business logic into code. This involves building a layer above data designed to emulate human behavior.

For example, in text matching, the goal is to accelerate tasks typically done by humans, such as researching and compiling data to make predictions. AI engineers strive to create systems that can perform these tasks as efficiently as humans.

Could you give some insights into what's on a typical to-do list for you?

Currently, my main focus is on improving text matching accuracy in our system. My task is to implement Retrieval-Augmented Generation (RAG) techniques, which include hybrid search, re-ranking, and new methods of data embedding. These techniques aim to improve our text matching accuracy. This task involves a lot of experimentation, implementing different systems, and optimizing them for better performance.

How can you in a simple way explain the difference between a purpose-built AI tool and a generic AI tool?

General AI tools, like GPT-3, are versatile. They can adapt to various tasks, such as classification or auto-completion. The interface is straightforward: input text, get text out. However, when you want the AI to use a specific language or guide a user in a certain way, prompt engineering becomes essential. People customize these general systems with specific instructions, but this can be cumbersome and has its limitations.

Purpose-built AI like Sixfold comes into play when you start fine-tuning the systems. This involves feeding them examples of data to achieve a desired tone, style, or structure. Additionally, building a knowledge retrieval system on your proprietary data can make your AI unique, providing access to information that other systems don't have. Customizing AI systems is challenging. It's one thing to create a demo or a cool AI video, but running these systems in a production environment, especially in enterprise-grade products, requires them to respond quickly, like within two seconds. So, a lot of work goes into customizing an AI system for practical, real-world applications.

What’s your take on transparency in AI, particularly with large language models?

I believe transparency is crucial in AI, both within and outside organizations. Particularly, I'm referring to how AI tools are built and used. Although we're not yet at a point where AI systems are making all decisions autonomously, the trend is moving towards AI taking over more complex tasks. Take self-driving cars as an example: in the future, human-driven cars might be considered less trustworthy or even costlier to insure compared to AI-driven ones, potentially limiting human driving to specific scenarios like racetracks.

In such cases, it becomes vital for the AI systems controlling these cars to be transparent. We need to understand their training data, be aware of their limitations, and identify potential risks, especially since these systems significantly impact society. This transparency is essential because AI systems are not deterministic; their output heavily depends on the quality of the input data. Understanding what an AI system has been trained on gives us a clearer picture of its capabilities and limitations, which is essential as these systems become more integral to our daily lives. That's how I view transparency in AI.

What excites you the most about Sixfold?

At my last role, my focus was on solving marketing problems, specifically automating marketing systems and content generation. Marketing is inherently subjective, which makes it challenging to capture the right flavor of content. One dilemma in this field is the risk of producing generic or misleading content, which can be detrimental to society.

The challenges in my current role are more complex. It's about understanding and utilizing the reasoning capabilities of the model, which involves deducing insights from a given set of data. This differs from just altering the tone of content for marketing purposes.

For example, in marketing, success is often measured by a feedback loop, like how much generated content is retained in a final document, indicating user preference. However, in my current role, the metrics are different. We have a known 'ground truth' or a specific outcome we aim to achieve, and the goal is to develop a system that consistently aligns with this known outcome. This requires a higher level of accuracy and a different approach compared to marketing, where the outcomes are more subjective and based on individual perception.

How do you stay updated with the advancements in AI and large language models? Are there any newsletters or blogs you follow?

It's one of the biggest challenges in this field! You might spend months developing something innovative, only to find it's made obsolete by a new development the following week.

It can be frustrating, but it's also exhilarating. You learn to not get too attached to your work and treat it as part of a learning journey. The field is dynamic; each week brings something new that could either render your current work obsolete or introduce an exciting new method.

However, it's crucial for companies to remain disciplined and not get constantly sidetracked by every new innovation. Deciding whether to try out new technologies and determining their integration importance requires careful consideration.

As for staying informed, I don't stick to specific newsletters or blogs. I prefer a more hands-on approach, as I'm not from an academic background. I find YouTube content especially useful for seeing how new things are implemented. It's more about application for me – I need to see something in action to understand it. So, I explore various sources like Hacker News and YouTube, or anything relevant I come across on a particular topic.

Do you share your own work or insights publicly?

Actually, I don't engage much in open source work or sharing my projects publicly. After work, I prefer to disconnect and focus on other interests, like learning guitar. It's about maintaining a healthy balance. I'm fortunate that my work aligns closely with my interests. Over the past three years, I've had the opportunity to explore new techniques and projects that I've been curious about, right in my professional environment. For instance, this week I'm working on an advanced retrieval system, something I've always wanted to try.

Considering young engineers or students interested in entering this field, do you have any advice or recommendations for them?

My main advice is that simply following tutorials and reading books isn't enough to truly learn. The key is to build something. You need to apply what you've learned, either in a professional setting or through a personal project. In technology, and especially in AI, hands-on experience is essential. The possibilities with AI are vast. Building on top of existing AI systems is surprisingly accessible.

For instance, I'm currently working on an AI-based pet project. It's essentially a photo translator using a Raspberry Pi device, which has a computer, display, and camera. The idea is that you take a picture of something, and the system uses GPT for vision to describe what it sees. Then, using that description, it generates a DALLE 3 image related to the object and displays it on the screen. I call it the 'Unreal Camera.' For example, if you take a picture of a dog, it creates an artistic interpretation of that dog. It essentially presents a graphic version of whatever you photograph.

This kind of project would have been impossible to undertake alone a few years ago; it would have required a whole team and several years. Now, thanks to the power of AI, I was able to build it in just two days. So, my recommendation for anyone entering this field is to start building something practical and useful. That's the best way to learn and understand the potential of AI.

Do you have a favorite AI tool at the moment?

I primarily use ChatGPT and a fascinating app called Perplexity, which is great for research. Perplexity is unique in how it can visit different websites and compile data. Another tool I frequently use is GitHub Copilot for coding. It's incredibly helpful, as it assists in writing code. These tools, especially Copilot, have been instrumental in my work.

Thanks for your time, Drew! We’ll let you get back to your AI tasks now.

If you’d like an opportunity to work at Sixfold, check out our vacancies.

FEATURED REPORTS

Business Intelligence Reports

Data-driven reports for smarter business decisions.