Built For How P&C Underwriters Actually Work

Sixfold learns your risk appetite, assesses submissions, and automates what comes next.

Underwriters' time is too valuable for hours of manual work.

Here's how Sixfold clears the admin and keeps underwriting moving:

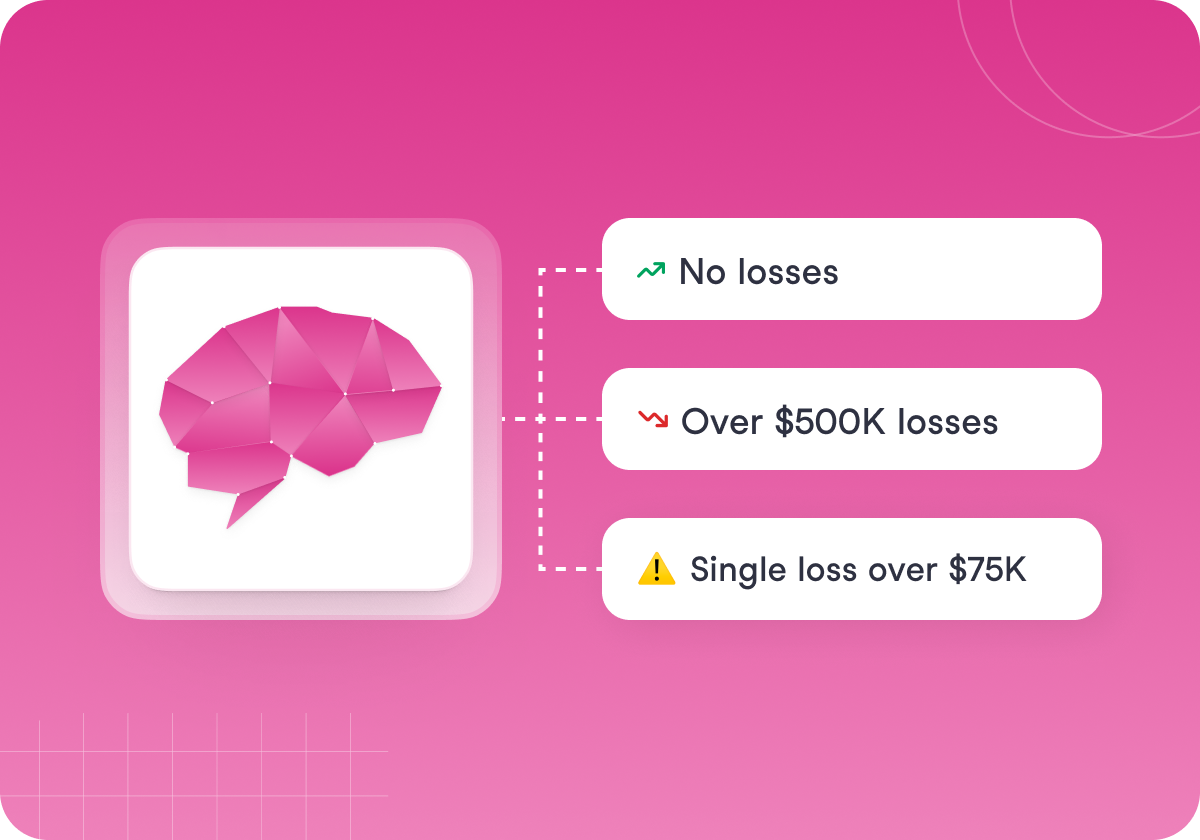

Understands Your Risk Appetite

Sixfold ingests your underwriting guidelines and learns your specific risk appetite—what to prioritize, what to flag, what matters most.

Underwriting brain tailored to your guidelines

Specific to each line of business you write

Easily update as risk appetite evolves

.png)

Analyzes Every Submission

Sixfold handles messy submissions as they come, no separate data extraction tools needed. Every submission gets read completely and assessed consistently against your appetite.

Ensures consistent guideline application

Surfaces risks buried deep in documents

Easy intake via direct upload, email forward, or API

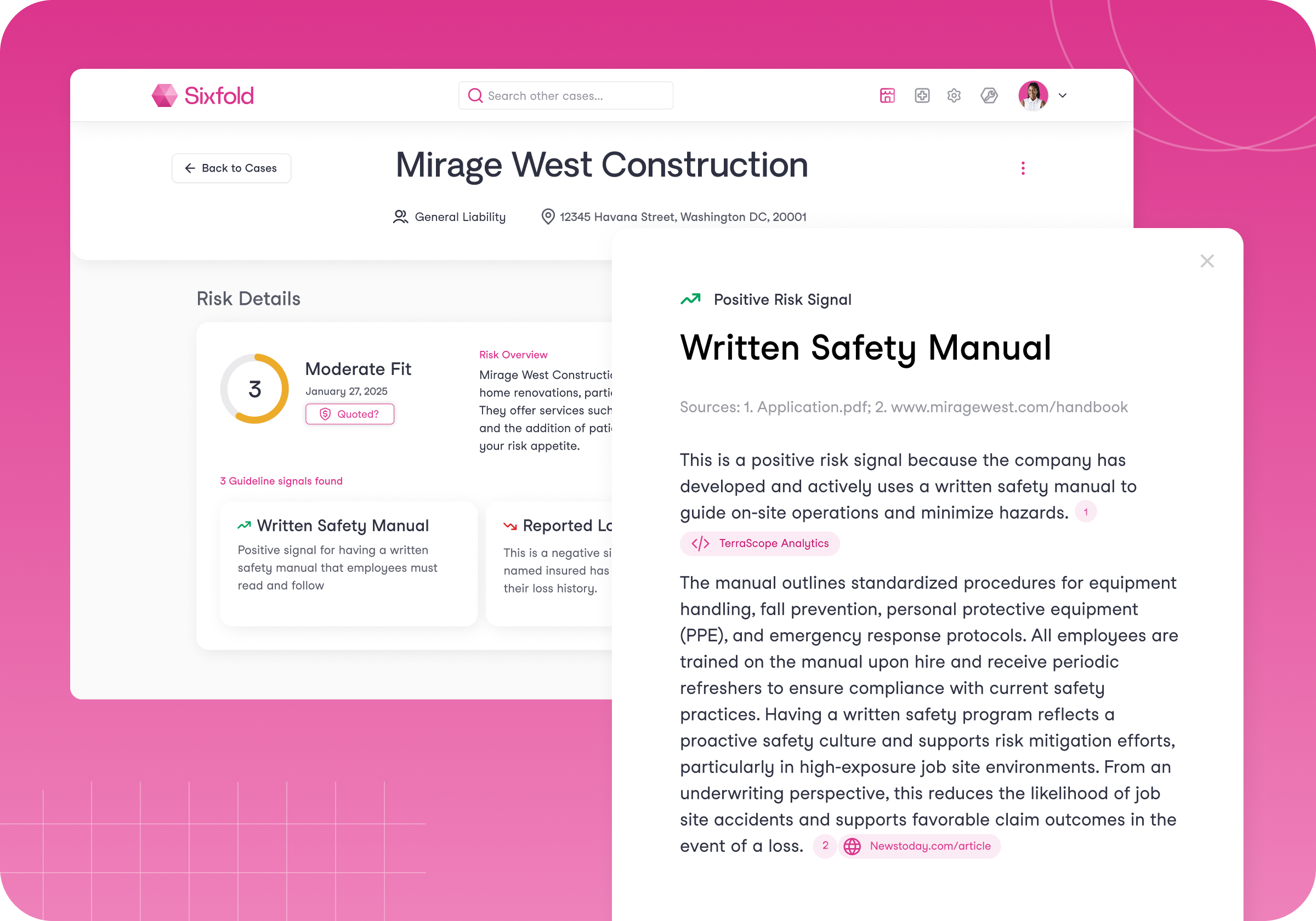

Surfaces What Matters Most

Sixfold surfaces appetite fit scores for quick triage, individual signals that explain the risks found and why they matter, and a full case narrative. All cited for easy verification and documentation.

Risk insights explained relative to your guidelines

Sources cited for easy verification and documentation

Flexible narrative format adapts to your workflow needs

.png)

Takes Action to Clear Bottlenecks

AI agents automate time-consuming tasks like research, referrals, and portfolio reviews so underwriters can focus on growth.

Pre-trained for common underwriting tasks

Deploy one agent or multiple

Agent outcomes displayed for human-in-the-loop

.png)

INTEGRATIONS

Works Wherever You Do

Use Sixfold standalone or our flexible API to integrate into your existing workbench, CRM, or policy admin system. Underwriters stay in familiar environments while AI works in the background.

Sixfold by the Numbers

1M+

submissions processed

40+

lines of business across P&C and L&H

50%

faster case reviews

30%

increase in premiums per underwriter

Some of our key capabilities

Accuracy

Analyzes and interprets data correctly to assess risks and make insurance policy recommendations.

Summarization

Condenses large volumes of data, documents, and information into reader-friendly summaries.

Fact Extraction

Extracts and highlights relevant pieces of data from a broad array of data sources.

Fact Inconsistencies

Identifies discrepancies within information collected from submissions, third party data and additional documents.

Risk Classification

Categorizes entities (SIC, NAICS, ISO, ICD, SNOMED)or individuals based on their level of risk.

Refinement

Enhances the precision of risk assessments by incorporating more detailed information.

Re-Ranker

Adjusts the prioritization of cases, highlighting those most aligned with the company's risk appetite.

Submission Triage

Appetite-aligned risk scores to prioritize submissions at a glance.

Risk Assessment

Risk signals and case narratives tailored to your guidelines to inform underwriting decisions.

Action Agents

AI Agents that make recommendations and take action to clear common underwriting bottlenecks.

Portfolio Management

Track risk patterns and broker performance to optimize your book of business.

Data Enrichment

Automated web and third-party research incorporated directly into risk assessment.

Transparent Citations

All sources cited for easy verification and documentation.

Business Classification

Categorizes entities or individuals according to industry standards (SIC, NAICS, ISO, ICD, SNOMED).

See why insurers love Sixfold

"Sixfold has become essential to our underwriting operations. We've gone from testing it to requiring its input for every quote."

Matthew Richardson

Global Head of Operations & IT @Generali GC&C

.png)

"Sixfold delivers insights to make fast and confident decisions, driving better engagement with brokers and customers"

Kristof Terryn

Chief Executive Officer @Zurich North America

.svg)

"Sixfold enhances underwriting insight, consistency, speed of analysis and response"

Andrew Robinson

Chairman & CEO @Skyward Specialty

.png)