If You’re Not Fast, You’re Late in E&S

Excess & Surplus insurance demand has surged over the past few years, and for underwriters, that means more cases to sort through every day. We’ve heard from professionals across the segment about how high the case volume has gotten and how challenging it is to keep up.

So what’s driving this? We’re talking about one of the fastest-growing lines in insurance, with a 21% compound annual growth rate over the past five years, according to Insurance Journal. The growth comes from the segment’s ability to handle uncertainty like economic shifts or environmental changes, which have gotten more complex in recent years.

We’re talking about one of the fastest-growing lines in insurance, with a 21% compound annual growth rate over the past five years

One example is a cannabis business trying to get insurance. That kind of risk wouldn’t even be considered a few years ago. Since E&S takes on the risks standard carriers won’t, it’s absorbing more business, especially as admitted carriers get more cautious with the economic changes. At the same time, wholesale brokers—experts in hard-to-place risks—are sending more business than ever to E&S carriers.

The market's growth has also led to increased participation from both newly-capitalized and re-capitalized insurers, as well as managing general agents entering the distribution side. This influx has intensified competition, resulting in a decline in market share for 14 of the top 25 E&S players in 2021, according to Risk & Insurance.

The Hidden Bottlenecks in Quoting

As the market surges, underwriters are buried in rising case volumes and more complex risks. With more players, competition, and pressure from wholesale brokers, getting quotes back quickly isn’t just nice to have–it’s critical for winning and retaining business. But what is currently causing delays in the quoting process?

As the market surges, underwriters are buried in rising case volumes and more complex risks

1. Many submissions, no easy way to filter them

E&S carriers receive all the non-admitted risks that standard insurers decline, often from a wide range of wholesale brokers. That volume adds up fast. The immediate impact? Underwriters have a hard time identifying the winnable opportunities and spend time working on cases that are out of their appetite.

2. Quoting process is mostly manual

A big part of the quoting process is manual. There’s a lot of data entry, systems that don’t help with prioritization, and information in all kinds of formats.

Because of that, E&S underwriters are still spending a lot of valuable time on manual tasks. In some cases, quoting can take up to 30 days. Think about incorrect routing between departments, incomplete information from brokers, and offshore teams handling SIC/NAICS code classification.

All of that slows everything down. And brokers? They’re expecting fast answers.

And brokers? They’re expecting fast answers.

3. Complex risks with tight deadlines

E&S risks are complex, and they take time to quote. But with the amount of submissions coming in, there’s just not enough time in the day to go through them all manually.

Underwriters need fast access to the key information that actually matters. That’s the only way to speed up quoting or quickly say no to risks that don’t fit.

The Result

All of this leads to premiums not being looked at, slower response times to brokers, and losing good deals to the competition. In a segment where demand is high and it’s nearly impossible to assess every risk, it’s key to spot high-quality submissions earlier in the process so carriers and underwriters aren’t stuck spending time on risks that won’t bind.

And when that happens, it’s not just GWP left on the table—it’s lost time and momentum.

Just think about the amount of premium carriers could capture by identifying the right opportunities from the start. Especially in a market that reached $130 billion in direct premiums in 2024 according to Insurance Insider US.

Imagine recieveing 50 submissions and already knowing which ones to prioritize, which ones fit your guidelines, what’s worth pricing creatively, and what’s a fast no

So, how can underwriters identify the right risks?

It all starts with quickly understanding whether a submission matches your appetite through an efficient triaging process. Imagine receiving 50 submissions and already knowing which ones to prioritize, which ones fit your guidelines, what’s worth pricing creatively, and what’s a fast no.

It’s not about writing any piece of business, it’s about writing the right ones for your business. With proper triaging, underwriters can move faster, get back to brokers quicker, and focus on what matters.

So, how do you actually get to the right risks faster? That’s where Sixfold comes in.

AI that Instantly Identifies Your Top Risks

Sixfold’s triage solution speeds up decision-making with instant, appetite-aligned scoring. Here’s how it works:

1. Showcasing the cases you want to quote

Sixfold ingests each insurer’s underwriting guidelines to learn the company’s unique risk appetite. Then, based on SOVs, applications, loss runs, and additional data, Sixfold’s AI runs the risk assessment, using both the documents uploaded and relevant company info it pulls from the web. It looks at the data points that matter for the insurer, such as for example construction year, occupancy, loss history, and more. From there, it generates a risk score for the submission from 0 to 5.

- 0 means it doesn’t fit your risk appetite at all

- 5 means it’s a highly qualified risk for you

Solving the front door issue by filtering risks immediately means underwriters can respond faster, whether it’s a quote or a decline

The impact? Underwriters know right away which incoming applications are worth their time. Wholesale brokers are strategic partners for E&S carriers. But when underwriters get too busy, they are sometimes left waiting for a reply. Solving the front door issue by filtering risks immediately means underwriters can respond faster, whether it’s a quote or a decline.

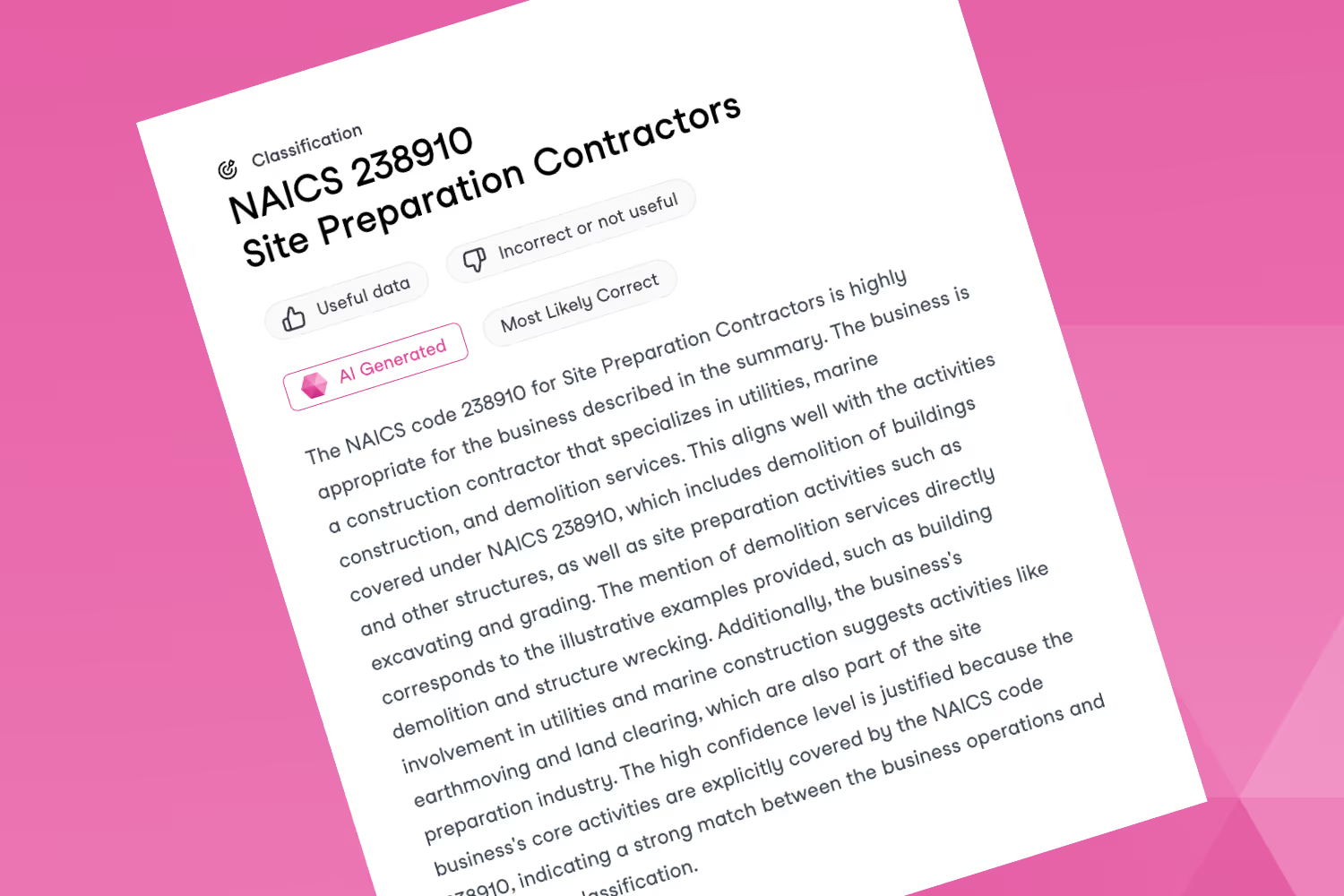

2. Classifying businesses with > 90% Accuracy

In E&S, sometimes a small difference in business activity can immediately make a risk fall out of the risk appetite. That’s why accurate NAICS and SIC code classification is key.

Sixfold automatically matches each submission to the correct business classification code, even for highly nuanced and complex industries, so no more time is wasted trying to figure out what type of business the company is. This supports better routing and faster underwriting decisions.

3. Presenting contextual risk factors

Sixfold surfaces the risk signals that matter most, whether they disqualify a submission, negatively impact it, or strengthen it. Everything is aligned with the insurer’s appetite and focused on the factors that drive the overall decision. Underwriters get precisely what they need to make confident calls.

Underwriters get precisely what they need to make confident calls.

See It in Action

The volume of submissions in E&S isn’t slowing down. But with the right triage process, underwriters can focus on decision-making, quote the right risks faster, and bring in more premiums.

The carriers winning today aren’t working harder; they’re triaging smarter.

Join our E&S product demo on May 21 with Alex Bontz, Customer Success Operations & Growth Lead. He’ll walk through how Sixfold quickly triages complex submissions and delivers the key risk insights underwriters need to take action.

Looking to catch up in person? Come find us at the E&S Reuters Conference on May 28. We will be there to connect with insurers looking for ways to improve their underwriting process with purpose-built AI.