Sixfold Content

Sixfold News

Sixfold Partners with Adnovum

Sixfold is teaming up with Adnovum, the Swiss technology and consulting company specializing in secure digital transformation for the insurance industry.

.png)

Stay informed, gain insights, and elevate your understanding of AI's role in the insurance industry with our comprehensive collection of articles, guides, and more.

AI in Insurance Is Officially “High Risk” in the EU. Now What?

The new EU AI Act defines AI in insurance as “high risk.” Here’s what that means and how to remain compliant in Europe and around the world.

The European Parliament passed the EU Artificial Intelligence Act in March, a sweeping regulatory framework scheduled to go into effect by mid-2026.

The Act categorizes AI systems into four risk tiers—Unacceptable, High, Limited, and Minimal—based on the sensitivity of the data the systems handle and the crucialness of the use case.

It specifically carves out guidelines for AI in insurance, placing “AI systems intended to be used for risk assessment and pricing in [...] life and health insurance” in the “High-risk” tier, which means they must continually satisfy specific conditions around security, transparency, auditability, and human oversight.

The Act’s passage is reflective of an emerging acknowledgment that AI must be paired with rules guiding its impact and development—and it's far from just an EU thing. Last week, the UK and the US signed a first-of-its-kind bilateral agreement to develop “robust” methods for evaluating the safety of AI tools and the systems that underpin them.

I fully expect to see additional frameworks following the EU, UK, and US’s lead, particularly within vital sectors such as life insurance. Safety, governance, and transparency are no longer lofty, optional aspirations for AI providers, they are inherent—and increasingly enforceable—facets of the emerging business landscape.

Please be skeptical of your tech vendors

When a carrier integrates a vendor into their tech stack, they’re outsourcing a certain amount of risk management to that vendor. That’s no small responsibility and one we at Sixfold take very seriously.

We’ve taken on the continuous work of keeping our technology compliant with evolving rules and expectations, so you don’t have to. That message, I’ve found, doesn’t always land immediately. Tech leaders have an inherent “filter” for vendor claims that is appropriate and understandable (I too have years of experience overseeing sprawling enterprise tech stacks and attempting to separate marketing from “the meat”). We expect—indeed, we want—customers to question our claims and check our work. As my co-founder and COO Jane Tran put it during a panel discussion at ITI EU 2024:

“As a carrier, you should be skeptical towards new technology solutions. Our work as a vendor is to make you confident that we have thought about all the risks for you already.”

Today, confidence-building has extended to ensuring customers and partners that our platform complies with emerging AI rules around the world—including ones that are still being written.

Balancing AI underwriting and transparency

When we launched last year, there was lots of buzz about the potential of AI, along with lots of talk about its potential downside. We didn’t need to hire pricey consultants to know that AI regulations would be coming soon.

Early on, we actively engaged with US regulators to understand their thinking and offer our insights to them as AI experts. From these conversations, we learned that the chief issue was the scaling out of bias and the impact of AI hallucinations on consequential decisions.

With these concerns in mind, we proactively designed our platform with baked-in transparency to mitigate the influence of human bias, while also installing mechanisms to eliminate hallucinations and elevate privacy. Each Sixfold customer operates within an isolated, single-tenant environment, and end-user data is never persisted in the LLM-powered Gen AI layer so information remains protected and secure. We were implementing enterprise AI guardrails before it was cool.

I’ve often found customers and prospects are surprised when I share with them how prepared our platform is for the evolving patchwork of global AI regulations. I’m not sure what their conversations with other companies are like, but I sense the relief when they learn how Sixfold was built from the get-go to comply with the new way of things–even before they were a thing.

It Takes You Months to Train AIs? You're Doing It Wrong

Discover the power of AI underwriting with Sixfold - the ultimate solution to overcome traditional limits and stay ahead in the insurance industry.

It’s impossible in 2024 to be an insurance carrier and not also be an AI company. In this most data-focused of sectors, the winners will be the organizations making the best use of emerging AI tech to amplify capacity and improve accuracy.

This is a challenge and opportunity that Sixfold is uniquely suited to address thanks to our decades of collective industry and technological experience. We know insurers’ needs—intimately—and understand precisely how AI can overcome them.

In previous posts, I’ve described how Sixfold uses state-of-the-art AI to ingest data from disparate sources, surface relevant information, and generate plain-language summarizations. Our platform, in effect, provides every underwriter with a virtual team of researchers and analysts who know exactly what’s needed to render a decision. But getting there is the rub. Training AI models (these “virtual teams”) to understand what information is relevant for specific product lines is no small task, but it’s where Sixfold excels.

To use AI is human, to create your own unique AI model is divine

Underwriting guidelines aren’t typically encapsulated in a single machine-readable document. They’re more likely to exist in an unordered web of internal documents and reflected in historic underwriting decisions. Distilling a diffuse cultural understanding into an AI model can take months using a traditional approach, but with Sixfold, it can be accomplished—and accomplished well—in as little as a few days.

Sixfold’s proprietary AI captures carriers’ unique risk appetite by ingesting a wide variety of inputs (be it a multi-hundred-page PDF of guidelines, a loose assortment of spreadsheets, or even past underwriting decisions) and translating it into an AI model that knows what information aligns with a positive risk signal, a negative one, or a disqualifying factor.

With this virtual wisdom model in place, the platform can identify and ingest relevant data from submitted documents, supplement with information from public and third-party data sources, and generate semantic summaries of factors supporting its conclusions—all adhering to the carriers’ unique underwriting approach.

Frees human underwriters to do uniquely human tasks

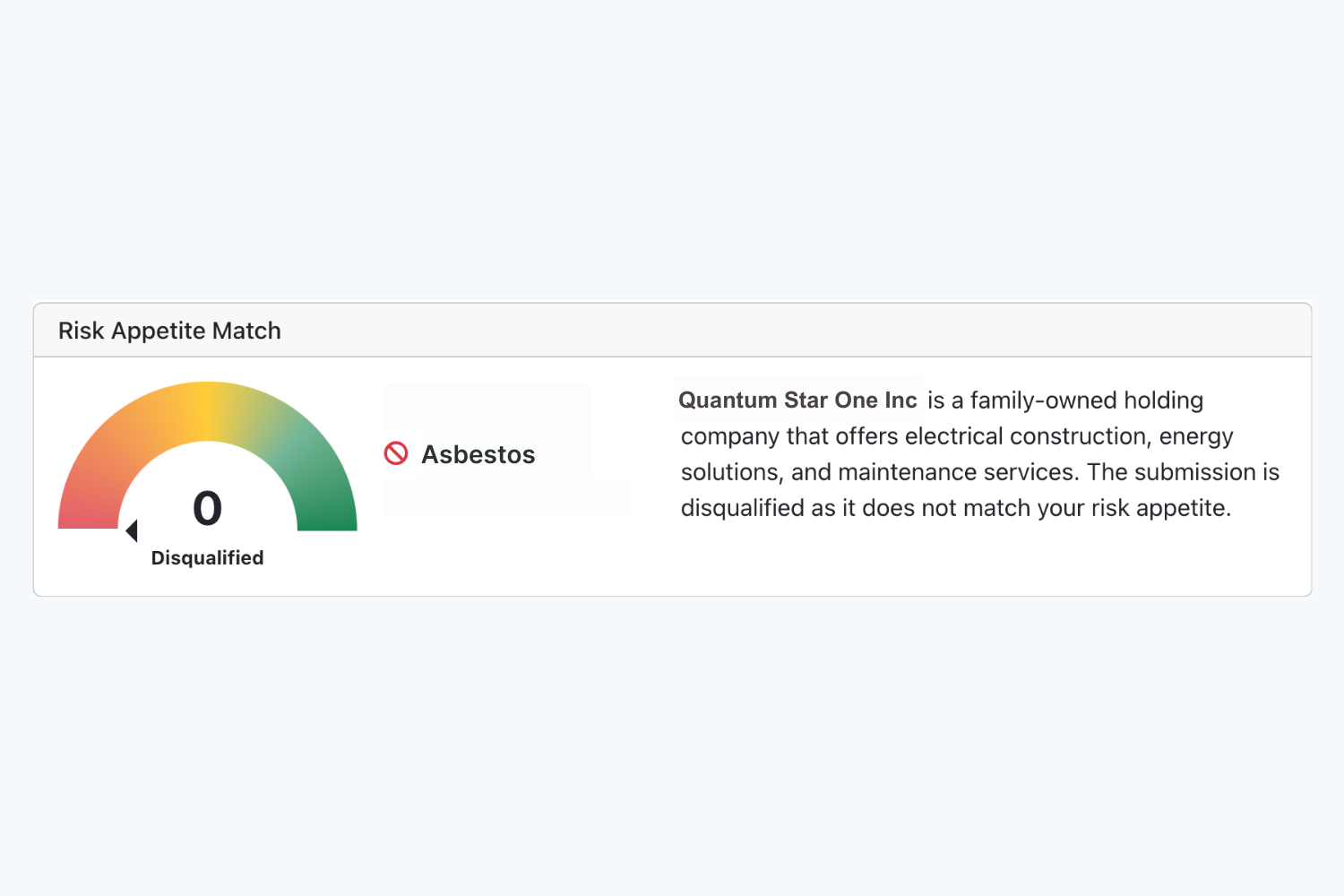

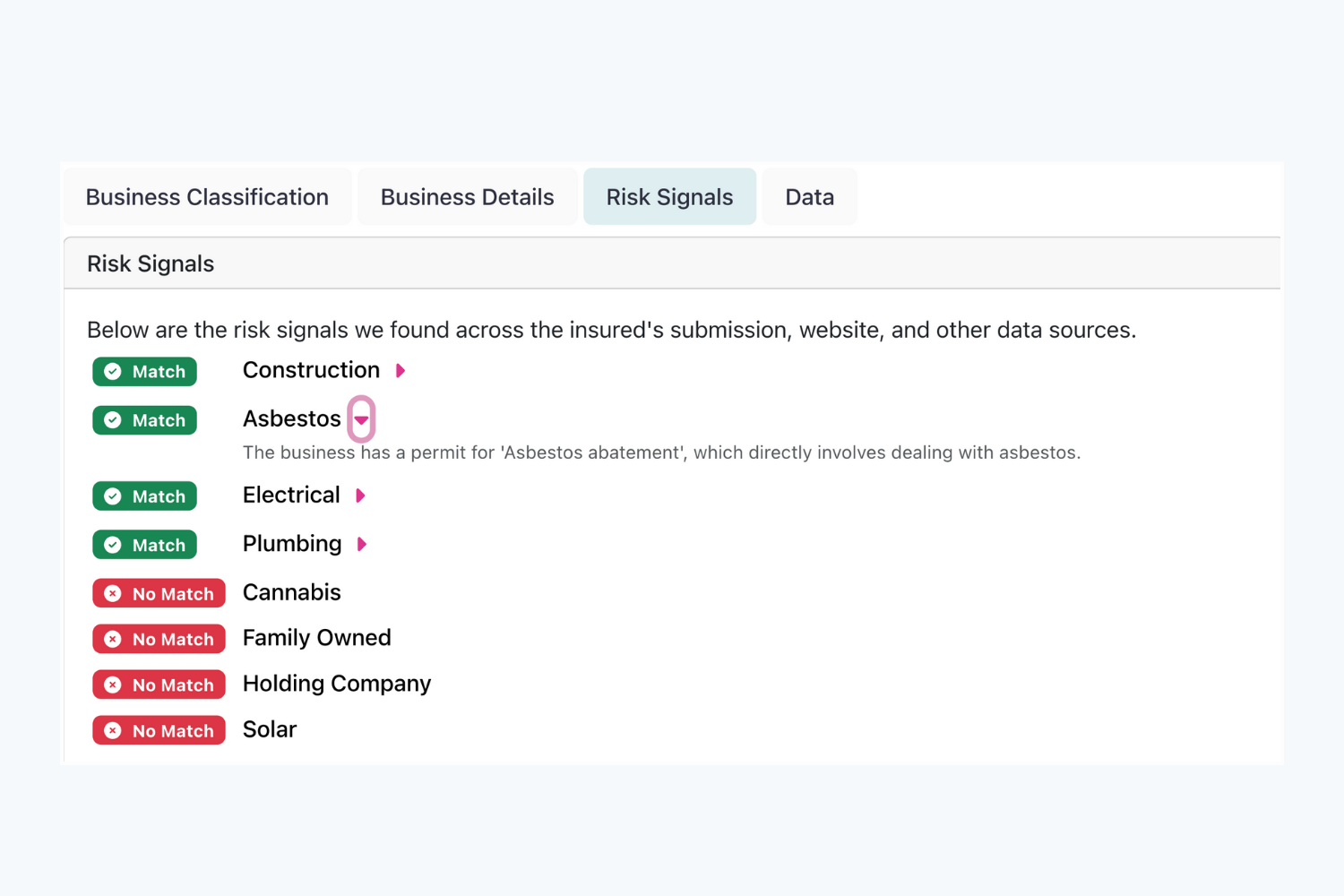

It can take years for a human underwriter to master underwriting guidelines and rules, but that doesn’t mean human underwriters are no longer needed–quite the opposite. By offloading the administrative bulk to AI, underwriters can use their increased capacity to prioritize cases that align with their unique risk appetite.

Consider a P&C carrier that prefers not to underwrite businesses that work with asbestos. When an application comes in, Sixfold’s platform processes all broker-submitted documents and supplements it with relevant data ingested from public and third-party data sources. If Sixfold were to then surface information about “assistance with obtaining asbestos abatement permits” from the applicant’s company website, it would automatically mark the finding as a negative risk signal (with clear sourcing and semantic explanation) in the underwriter-facing case dashboard. With Sixfold, underwriters can rapidly discern the applications that are incompatible with their underwriting criteria and quickly focus on cases aligned with their risk appetite.

Automating these previously resource-intensive data processing workflows allows carriers to obliterate traditional limits on underwriting capacity. The question for the industry has rapidly moved from “is automation possible?” to “how quickly can we get it implemented?” Sixfold’s purpose-built platform empowers customers to leapfrog competitors relying on traditional approaches to training AI underwriting models. We get you there faster–this is our superpower.

Navigating Unwritten Regulations: How We Did It

As regulators at all levels of government are drafting rules guiding the usage of artificial intelligence, Sixfold AI built a platform for unwritten rules.

AI is the defining technology of this decade. After years of unfulfilled promises from Hollywood and comic books, the science fiction AI future we’ve long been promised has finally become business reality.

We can already see AI following a familiar path through the marketplace similar to past disruptive technologies.

- Stage one: it’s embraced by early adopters before the general public even knows it exists;

- Stage two: cutting-edge startups tap these technologies to overcome long-standing business challenges; and then

- Stage three: regulators draft rules to guide its usage and mitigate negative impacts.

There should be no doubt that AI-powered insurtech has accelerated through the first two stages in near record time and is now entering stage three.

AI underwriting solutions, meet the rule-makers

The Colorado Department of Regulatory Agencies recently adopted regulations on AI applications and governance in life insurance. To be clear, Colorado isn’t an outlier, it’s a pioneer. Other states are following suit and crafting their own AI regulations, with federal-level AI rules beginning to take shape as well.

The early days of the regulatory phase can be tricky for businesses. Insurers are excited to adopt advanced AI into their underwriting tech stack, but wary of investing in platforms knowing that future rules may impact those investments.

We at Sixfold are very cognizant of this dichotomy: The ambition to innovate ahead, combined with the trepidation of going too far down the wrong path. That’s why we designed our platform in anticipation of these emerging rules.

We’ve met with state-level regulators on numerous occasions over the past year to understand their concerns and thought processes. These engagements have been invaluable for all parties as their input played a major role in guiding our platform’s development, while our technical insights influenced the formation of these emerging rules.

To simplify a very complex motion: regulators are concerned with bias in algorithms. There’s a tacit understanding that humans have inherent biases, which may be reflected in algorithms and applied at scale.

Most regulators we’ve engaged with agree that these very legitimate concerns about bias aren’t a reason to prohibit or even severely restrain AI, which brings enormous positives like accelerated underwriting cycles, reduced overhead, and increased objectivity–all of which ultimately benefit consumers. However, for AI to work for everyone, it must be partnered with transparency, traceability, and privacy. This is a message we at Sixfold have taken to heart.

In AI, it’s all about transparency

The past decade saw a plethora of algorithmic underwriting solutions with varying degrees of capabilities. Too often, these tools are “black boxes” that leave underwriters, brokers, and carriers unable to explain how decisions were arrived at. Opaque decision-making no longer meets the expectations of today’s consumers—or of regulators. That’s why we designed Sixfold with transparency at its core.

Customers accept automation as part of the modern digital landscape, but that acceptance comes with expectations. Our platform automatically surfaces relevant data points impacting its recommendations and presents them to underwriters via AI-generated plain-language summarizations, while carefully controlling for “hallucinations.” It provides full traceability of all inputs, as well as a full lineage of changes to the UW model, so carriers can explain why results diverged over time. These baked-in layers of transparency allow carriers–and the regulators overseeing them–to identify and mitigate incidental biases seeping into UW models.

Beyond prioritizing transparency, we‘ve designed a platform that elevates data security and privacy. All Sixfold customers operate within isolated, single-tenant environments, and end-user data is never persisted in the LLM-powered Gen AI layer so information remains protected and secure.

Even with platform features built in anticipation of external regulations, we understand that some internal compliance teams are cautious about integrating gen AI, a relatively new concept, into their tech stack. To help your internal stakeholders get there, Sixfold can be implemented with robust internal auditability and appropriate levels of human-in-the-loop-ness to ensure that every team is comfortable on the new technological frontier.

Want to learn more about how Sixfold works? Get in touch.

We at Sixfold believe regulators play a vital role in the marketplace by setting ground rules that protect consumers. As we see it, it’s not the technologist’s place to oppose or confront regulators; it’s to work together to ensure that technology works for everyone.

The Unspoken Truth: InsurTech AI's Struggle to Keep Up

Sixfold's state-of-the-art insurtech AI revolutionizes the insurance industry, tackling today's challenges head-on and preparing for the future.

The past decade saw more than its fair share of insurtech solutions promising to harness the power of “AI.” Many of these tools use hard-to-train algorithms powered by technologies that are years—if not decades—old. These legacy underwriting tools may inject some process efficiencies but don’t address the fact that insurers are struggling more than ever to expand capacity and grow Gross Written Premiums (GWPs) per underwriter.

Underwriters face a lot of issues

A recent Accenture survey found that underwriters spend 40% of their time on administrative tasks—that’s a full two days of their work week. Inboxes are flooded with more submissions than ever, but by some estimates, underwriters are only able to respond to 10%.

These aren’t challenges that companies can simply spend their way around; they require a fundamentally new approach. At Sixfold, we believe ascendent technologies, like LLM-powered generative AI, will lead the way. By moving beyond legacy solutions, carriers can take on today’s most pressing underwriting challenges–and the challenges on the horizon.

Ingesting and synthesizing data from disparate sources at scale

In the connected-everything world, insurers have access to more data than ever. This is a blessing and a challenge. On one hand, it guides decisioning and improves outcomes. On the other hand, there’s so much data from so many disparate sources, that it’s impossible to process efficiently.

Underwriters often find themselves sorting through hundreds of pages of documents for a single application. This limits capacity and squeezes GWP per underwriter. The only way to overcome these chokepoints without massively expanding headcount (and dinging already precarious expense ratios) is by using sophisticated AI tools to automate complex business tasks at scale.

With Sixfold’s state-of-the-art underwriting AI, insurers can seamlessly integrate structured and unstructured data from multiple disparate sources. The platform reflects each company's unique risk appetite, so it automatically surfaces relevant information to accelerate UW decisioning.

Say it in plain language

Sixfold uses LLM-powered generative AI (the same tech behind ChatGPT, Bard, etc.) to summarize findings to underwriters in plain language, not spreadsheets.

The platform, in effect, gives every underwriter their own virtual research team to build detailed reports on every application. Sixfold even generates coverage recommendations based on the company’s UW format. Compare this to legacy AI tools, which merely repackage information into number-heavy spreadsheets and dashboards, inevitably requiring additional inspection and contextualization from underwriters.

Even better? Plain language summations expand the underwriting talent pool by de-emphasizing technical and computational skillsets that are better handled by machines anyway. This is a crucial break from legacy tools, as insurers are now forced to compete for limited underwriting talent against private-equity-backed firms, insurtechs, MGAs, and other nontraditional insurance companies.

Opacity in insurance is no longer an option, AI transparency is the new norm

Sixfold was designed with transparency at its core because that’s what today’s customers expect and increasingly what regulators demand. The platform provides full sourcing and lineage of all underwriting decisions with clear semantic summaries, i.e. no more “black boxes.”

.png)

Customers accept automation as part of the modern digital landscape, but that acceptance comes with expectations of transparency, particularly when there are unexpected outcomes. Legacy solutions make it difficult—if not impossible—for insurers to provide customers with the clarity they deserve. Disappointed customers and diminished brand reputation, however, aren’t the only negative outcomes the industry needs to be mindful of.

As scaled automation becomes more ubiquitous, so have the calls for greater transparency from . At all levels of government, there are movements to counter the influence of potential bias through increased transparency and accountability—particularly in crucial areas like insurance.

The marketplace has long since moved on from “because the algorithm said so,” and insurers must employ tools to reflect those changes.

Beyond legacy AI

We’re not the first to automate underwriting tasks using “AI,” but we’re the first to fundamentally reimagine the underwriting role using state-of-the-art LLM tech to generate business value. Customers are using our platform to accelerate submission-to-quote cycles by as much as 43% and massively increase their GWP per underwriter.

The role of the underwriter is evolving, and the industry needs a new generation of tools to match. This is why we created Sixfold.